First Home Super Saver Scheme – update

CATEGORIES:

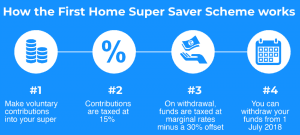

1st July 2018 is the milestone date that enables individuals to apply to withdraw voluntary contributions – made to super after 1 July 2017 – for a first home deposit, under The First Home Super Saver Scheme .

The scheme – part of Scott Morrison’s 2017 budget measures was designed to assist first home buyers save for a deposit in a tax effective way, without eroding their superannuation guarantee contribution. They do this by making voluntary contributions to their superannuation account that are able to be withdrawn to be used as a home deposit.

Voluntary contributions include:

Individuals may contribute up to $15,000 a year (which is included in their existing contribution cap), and up to $30,000 all-up over their lifetime. In a First Home Super Saver Scheme, tax is paid at 15 per cent on contributions. This means 85 per cent of the pre-tax contribution is put to work within the fund, earning a deemed rate of return equivalent to the 90-day bank bill rate plus 3 per cent.

The client is then allowed to withdraw a maximum of $30,000 in voluntary contributions, plus deemed earnings, to finance the purchase of their first home.

Concessional contributions and earnings that are withdrawn will be taxed at marginal rates less a 30 per cent offset.

For couples, both individuals can take advantage of the scheme.

For more information you can visit the ATO site

Anthony Landahl | Equilibria Finance

This is for general information purposes only and does not constitute advice. With all of these options there are a number of considerations outside the scope of what is covered in this article that you need to understand to ensure your personal circumstances are taken into consideration.